|

| Used with Permission |

One question I believe it is important to answer about any investment is "How do I get rid of it?" You never know what life will bring, or how the investment will do and if you don't know how to get out of an investment you may hold it too long or, to put it another way, you may not have your money where you need it when you need it. With Lending Club notes you can get your money out in two ways: withdrawing the monthly payments or selling the notes.

Each note hopefully has payments made each month. You can either reinvest these payments or withdraw them. While withdrawing the payments is the slow method to liquidating your investment (depending on when you invested and in what, it could take up to 60 months); it is simple and, assuming your borrowers don't default, you will get out of the investment what you bargained for when you bought it.

There is a secondary market for the notes as well, and that is the focus of this article. Once you are logged into your Lending Club account, you will see a link for a trading account. That will take you off Lending Club's site to a site by Folio Investors.

This is a screen shot from the front page of my Lending Club account. I'll talk more about what the numbers mean in another post. You'll see that I circled the link to the Trading Account. If I click, I am brought to this screen:

This is a screen shot from the front page of my Lending Club account. I'll talk more about what the numbers mean in another post. You'll see that I circled the link to the Trading Account. If I click, I am brought to this screen:

Logging into the secondary account:

The circles show that you can buy or sell notes.

Selling notes:

If you want to sell a note, whether it is because you no longer believe that note is a good investment or because you just want to get your money out to use for other things, you have to decide how to price that note. Folio is going to charge the seller a 1% commission on the sale, so at the least, if everything is going well with the note, you want to start by asking at least 1% more than the principal value (which will be shown to you on the "Sell" screen. (click screen shots to enlarge)

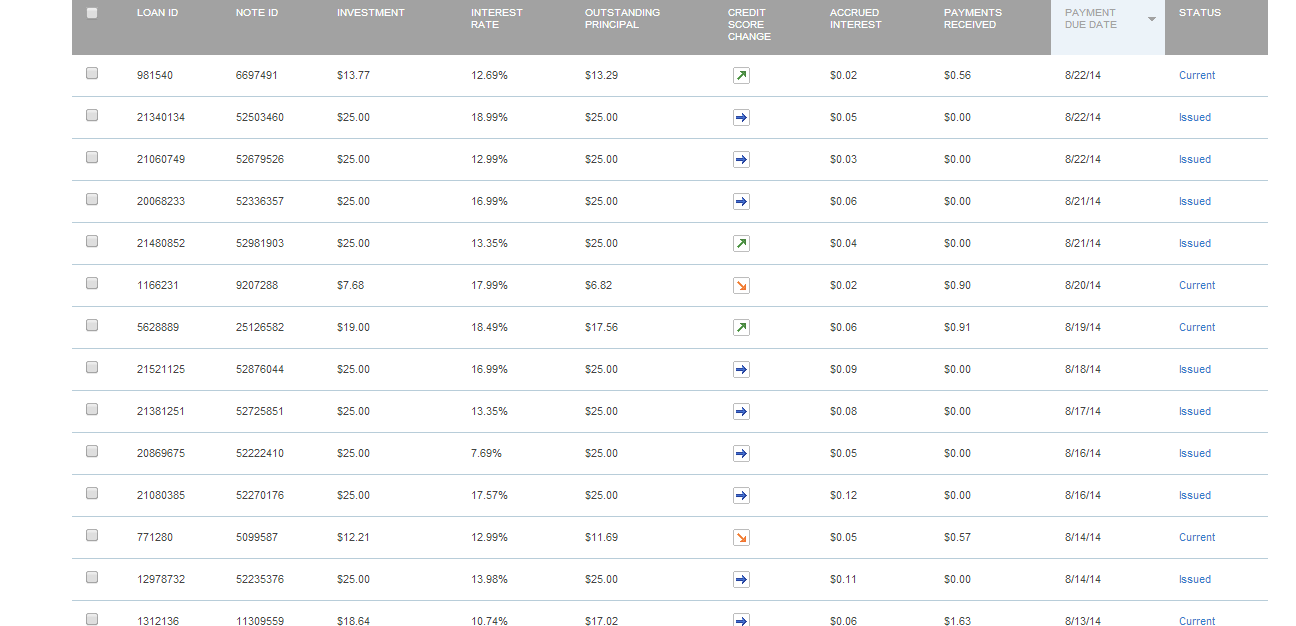

This screen shot shows the beginning of my list of notes. If you click on it, you will see how much I spent for the note (and yes, right now there are some for which I may have overpaid, but we'll see), the interest rate, the outstanding principal, how the borrower's credit rating has changed (or not) since the inception of the loan, the payments I have received on the loan, and when the next payment is due. All I have to do is click the box next to the loan I want to sell (and in this case, I'm not selling, just showing you how to do so).

If you compare this screen shot with the prior one you will see that I am trying to sell the top three notes. The columns on the right side of the screen are the ones I can manipulate. I can either choose an asking price or a mark-up/discount. In this case you can see by looking at the original list of notes that I am trying to sell a note with an interest rate of 12.69% that has remaining principal of $13.29 and that has a borrower whose credit rating is higher now than when the loan was originated. I am also trying to sell two $25.00 notes, one at 18.99% and the other at 12.99%, Once I add in a 1% mark-up to the first two notes, their yield drops to 10% and 17.2% respectively. That yield takes into account not only my mark-up but also the Lending Club commission of 1% of all payments collected. For example purposes, I listed on of the $25.00 notes at a discount, so you can see that the yield is still below the stated interest rate. If I was serious about doing this, I'd hit the "Submit" button and those notes would be available, at that price, for a week, unless they were purchased, or I decided to keep them, or I decided to change the price.

How much should I ask for the notes?

That depends on why you are selling, how badly you want to get rid of them, and how much work you want to put into this process. As I am writing this, there are 99,419 notes for sale. If I want mine to sell, I have to make it attractive to someone who is searching for a note to buy. I'm going to do a post later on buying notes, but suffice to say that most investors want to make money and the way you make money in this investment is by getting a high interest rate and by avoiding defaults. If those searching for a note to buy perceive yours as helping them meet that goal, it will sell. Otherwise, it will sit. In the cases above, my first note might get someone's attention--10% isn't a bad yield and the borrower has been making regular payments for some time and his credit rating is better now than when the loan started. The first $25.00 note might sell, or it might not. There is no payment history, so the new lender knows nothing I don't. The interest rate is high, which is a plus, but if you are in a state that allows it (some states don't allow you to purchase new notes), you can buy one like it at face value on the Lending Club site. Some people buy notes strictly with the idea of reselling them at slightly more than a 1% mark-up to people in states that don't allow direct purchase. If a note has a borrower whose credit rating has decreased, you aren't going to be able to get as much as one where the credit rating has increased. Poor payment habits also decrease the resale value of the notes, and good payment habits over nine or ten months can increase it since lenders see default as less likely at that point. In short, the law of supply and demand prevails. If your notes aren't selling you have the choice of keeping them, or lowering the price.

Which notes should I sell?

Again, that depends. Some people make money buying and selling notes. They (obviously) try to buy notes they consider underpriced, and to sell them for more. I read one blog post in which the author said he puts his notes up for sale every month after they pay interest. He always marks them up to what he calls a "make me sell it" price and figures that if people want to pay it, he is glad to take it. That sounds like too much work for me, though I have sold a couple of notes at a profit.

Some sellers are trying to raise cash. My guess is that the easiest way to do that is to sell high interest loans that have a good payment history. You may even be able to get a premium for them.

Some sellers are trying to dump loans they are afraid will go bad and offer them at discounts so as to attract bargain hunters.

Knowing that I can get at least part of my money out of an investment in relatively short order is important to me and the trading platform gives liquidity to my Lending Club investment.

No comments:

Post a Comment